How to fix the home price-income imbalance

The middle class suffocates under taxes

Advances in the realm of economics don’t often make the news. But it’s possible you’ve heard of Thomas Piketty’s Capital in the 21st Century, the economics book that took the world by storm in 2014. If you haven’t heard of Piketty’s research, then you’ve certainly heard of its main topic: wealth inequality.

Piketty’s thesis is crisp: return on capital grows more quickly than economic growth. Drawing this out to its natural conclusion, individuals who inherit substantial wealth see their assets increase more quickly than those relying on wage increases. Thus, wealth inequality will continue to grow between:

- those who labor for a living (the debtor class); and

- those who rely on investments for a living (the rentier class)

– unless regulations are altered, most likely through changes in the tax code. Property tax and Inheritance tax quickly come to mind.

Most relevant to real estate is Piketty’s idea that members of the middle class are being taxed exorbitantly on their greatest source of wealth: their homes. Piketty points out that we tax property in the U.S. without respect to actual accrued wealth. Taxation is based on the face value of the property, instead of the amount of the owner’s home equity – their wealth and capacity to pay.

An illustration

Consider two people who each purchase a $500,000 home. One owner liquidates stock to pay cash for the home. The other person put 3.5% down and has a job to support payments on a $480,000 mortgage balance ($20,000 in equity).

Taxwise, both are treated the same, even though they have two very different wealth profiles – capacity. (The exception is of course the mortgage interest deduction, which the owner paying all cash is not privy to, but that issue is a different discussion.)

Compounding the inequality is the fact that wealthy households have many nest eggs, thus ensuring not all their eggs are in one basket. Middle-class Americans often only have a single nest egg: their homes. Matthew Yglesias, writing for Vox, puts it this way:

Historically speaking, real estate has been taxed more heavily than other kinds of wealth because you can’t hide a house or shift it to an offshore account in the Cayman Islands. In contrast, state and local governments lack the technical capacity to tax mobile wealth like stock portfolios.

Thus, there are checks put in place by local and federal governments that in one sense keep incomes of middle-class homeowners in check. For the rentier class, these rules are bulleted with loopholes that lawmakers refuse to acknowledge, much less close.

The critique

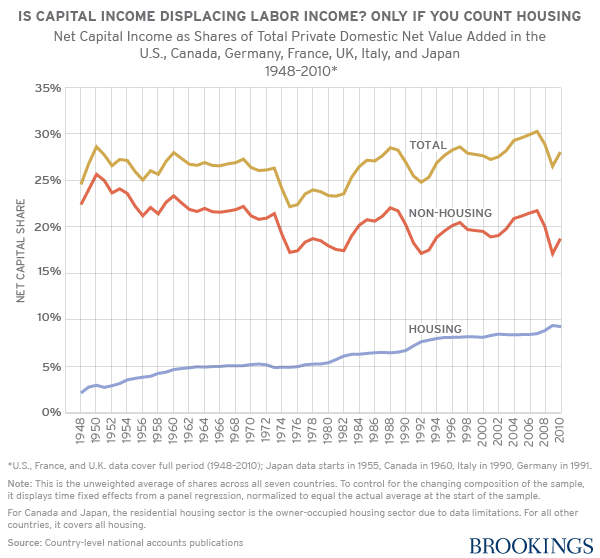

However, if you examine the growth wealth in capital – across the much of the world – over the past 60+ years, you’ll notice that most of this growth was actually seen in the housing sector. Take a look:

Source: Matthew Rognlie: Deciphering the fall and rise in the net capital share. Brookings Papers on Economic Activity.

In the chart above, you can see how property values have risen steadily as a share of total wealth over the past several decades. Other types of capital as a share of total wealth vary more wildly from year to year, but have actually declined slightly over this same time period.

This chart’s author, Matthew Rognlie, claims that Piketty’s analysis – which pits debtor against rentier in a competition for wealth that the rentier class continues to win – is flawed. Instead, Rognlie suggests we just forget about the rentier class, as their slice of the economy has no bearing on the rest of us, the 99%. As he says: “Observers concerned about the distribution of income should keep an eye on housing costs.”

The imbalance between home prices and wages

Indeed, housing costs have risen far more quickly than incomes in the past several years. Lenders and landlords alike recognize the ideal maximum a household should be spending on monthly rent (or mortgage payment) is roughly one-third of their monthly income. However, average housing costs are far beyond that in the areas where most of California’s residents live, at:

- 47% in Los Angeles;zonin

- 41% in San Francisco;

- 40% in San Diego; and

- 36% in Riverside.

How have housing costs gotten so out of control? From 2000 to 2013, real income(that’s income after inflation) rose 4%. Real home prices rose an incredible 75% in California over the same period.

Related article:

As more households are pouring a bigger share of their incomes into housing costs, less money remains to be contributed to the consumer economy, or saved. The savings rate has declined, to only 4.6% at the end of 2014, down from a peak of over 12% in the 1970s before mortgage deregulation set in. Naturally, this makes saving up for a needed down payment problematic, suggesting no end is in sight to this vicious cycle.

The solution

So, how to fix this big ol’ economic mess we’ve gotten ourselves into?

If you ask Piketty, it starts with helping the middle class overcome their unequal tax burden. This means taxing property based on its equity and not on the property’s fair market value, a “simple” change to the tax code.

On the other hand, Rognlie suggests we tackle property values themselves. The most realistic way to do this is to alleviate situations where demand outstrips supply, as most often occurs in urban areas and especially California (Texas producing the opposite result).

Keeping up with housing demand in urban areas not only brings housing costs more in line with wages, but enhances the entire economy. For instance, employment in and around San Francisco has the potential to increase by 500% without the legal restraints of zoning on new construction, according to the Economist. To translate, a more vibrant economy and more housing means a higher homeownership rate and greater home sales volume. Further, local tax revenues from property and sales will greatly increase, allowing local governments to meet community demands for classic services.

To achieve this goal, it means changing zoning codes.

The obstacle facing both of these solutions is that money talks loudly, very loudly to the exclusion of the middle class. Those with money have stakes in keeping certain loopholes firmly in the tax code and in controlling their neighborhoods from competitive growth. These advocates for restrictive zoning are often referred to asNIMBYs (not in my backyard advocates). But it is the resulting rush in property prices made by restrictive zoning that controls the thinking of NIMBYs, not community needs.

One thing’s for certain: nothing will improve if we adhere to the status quo.

First, we need a shift in attitude. Placing the rentier and debtor class in competition won’t initiate change (the debtor class lacks the money needed for this type of distinctive transformation).

Instead, let’s work for the same end. Surely members of the rentier class don’t want to return to a world without a middle class — that would make for a pretty poor economy, and unstable protest movements to boot.

Once we get on the same page about financially healthy shelter needed by newcomer households, businesses and government agencies, we can begin to work toward a shift in policy. If you agree, you need to let your voice be heard by participating with members of your local city councils and planning commissions to affect density through zoning change:

No comments:

Post a Comment